Návrh zákona amerického prezidenta Donalda Trumpa o daních a výdajích by americkým společnostem zabývajícím se kritickými minerály zkomplikoval konkurenci s Čínou, protože ruší daňové úlevy na podporu domácí produkce niklu, vzácných zemin a dalších materiálů používaných v moderní elektronice a zbrojním průmyslu.

Vzhledem k tomu, že Trump a republikánští zákonodárci usilují o snížení vládní podpory projektů v oblasti zelené energie, americká Sněmovna reprezentantů minulý měsíc schválila verzi jeho „One Big Beautiful Bill Act“, která ruší takzvanou 45X úlevu. Senát nyní o návrhu zákona diskutuje.

Zákon o změně klimatu z roku 2022 bývalého prezidenta Joea Bidena, Inflation Reduction Act, zavedl 10% úlevu na dani z výroby – snížení daně z příjmu právnických osob pro těžbu a zpracování kritických minerálů. Daňová úleva se vztahuje také na projekty v oblasti solární, bateriové a větrné energie.

Verze zákona, která prošla Sněmovnou reprezentantů, zachází s vládními pobídkami pro větrné turbíny stejně jako s pobídkami pro těžební projekty, které mnozí považují za klíčové pro národní bezpečnost. Společnosti zabývající se kritickými minerály nyní tvrdí, že jejich projekty jsou vedlejším produktem politického sporu o obnovitelné zdroje energie.

Daňová úleva je již zákonem a součástí aktuálního federálního rozpočtu. Nezávislá Kongresová rozpočtová kancelář, která na žádost Kongresu vyhodnocuje náklady legislativních návrhů, nezkoumala, kolik by se zrušením úlevy ušetřilo.

Republikánská většina v Kongresu hledá úspory na financování jiných priorit, jako jsou snížení daní, obrana a vyrovnání rozpočtu. Tento měsíc tvrdě pravicová frakce Sněmovny reprezentantů Freedom Caucus prohlásila, že „nepřijme“ pokusy „oslabit, odstranit nebo zrušit těžce vybojované škrty výdajů a zrušení zeleného podvodu IRA, kterých bylo dosaženo v tomto zákoně“.

As a result of everything discussed in the previous overviews, the spike in oil and gas prices will undoubtedly be reflected in prices across America, Europe, and the world. This is inevitable. Central banks will have to shelve their "dovish" plans, and some may even need to resume tightening monetary policy. Regarding Trump's triumphant march across the Earth, I see no resolution other than an announcement by the American president of an unconditional victory.

I remind you that Trump decides when to start a war (and for what reasons) and when to end it (and for what reasons). In many situations, the American president prefers intimidation. If this method does not work, bluffing begins. For example, outrageous tariffs or sanctions that eventually decrease to quite manageable, yet still favorable levels for America. If this tactic also fails, Trump counts on a military blitzkrieg—namely, a quick intervention. This was the case in Venezuela, and it is likely to happen in Cuba and other Latin American countries. After all, the ambitions of the US president do not end with Venezuela and Iran. Sometimes it seems that Trump has a list of several dozen countries that need to be "tamed," and that he systematically goes through it.

Returning to the Federal Reserve, the next meeting is scheduled for this week, but the markets are more interested in the outlook rather than the March outcomes. It is expected that the FOMC will significantly soften its "dovish" intentions and will be ready to lower the interest rate only once throughout 2026. This is all very good, but what about Donald Trump, who continues to demand that the Fed ease policy to the lowest possible levels? And it must be acknowledged that the economic statistics are currently on Trump's side. The American economy is slowing, the labor market shows no signs of recovery, and by May, the FOMC will have at least one more "dove" than it does now.

Therefore, I would not be so sure that the Fed's "dovish" intentions will truly weaken. Right now, the Fed is demonstrating the importance of preventing a renewed acceleration of inflation, but by May, the weakening labor market and the disappointing outlook for a US recession may come to the forefront. Especially if the war in the Middle East continues. Trump continues to claim that America benefits greatly from high oil and gas prices, yet American consumers are not thrilled with this. The state and government collect the revenue, while American consumers are forced to pay more at gas stations and stores. If this continues, the Republicans may lose control of both houses in November.

Based on my analysis of EUR/USD, I conclude that the instrument remains within an upward segment of the trend (lower chart), but in the short term, it has begun forming a downward segment of the trend. Since the five-wave impulse structure has been completed, my readers can expect a price increase over the next week or two, with targets around 1.1568 and 1.1666, which correspond to the 23.6% and 38.2% Fibonacci levels. Further movements of the instrument fully depend on developments in the Middle East.

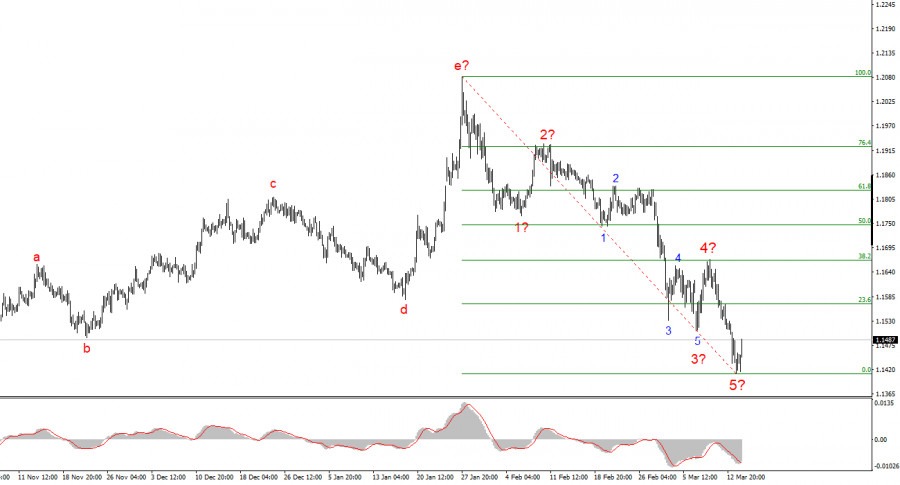

The wave picture of the GBP/USD instrument has become very complex and difficult to read. We now see a seven-wave downward structure on the charts, which is certainly not such. Most likely, there is an extension or complication within one of the waves. However, this does not make the wave count clearer. If the wave picture has once become complicated to the point of unreadability, it can become complicated again several times. Therefore, I believe that one should currently rely on the wave count of the EUR/USD instrument, which looks much more understandable. Also, do not forget the geopolitical factor, which can send both instruments into a new decline at any time. If this does not happen, the euro and the pound may see a slight increase within the context of a correction.

ລິ້ງດ່ວນ

ForexMart is authorized and regulated in various jurisdictions.

(Reg No.23071, IBC 2015) with a registered office at First Floor, SVG Teachers Co-operative Credit Union Limited Uptown Building, Corner of James and Middle Street, Kingstown, Saint Vincent and the Grenadines

Restricted Regions: the United States of America, North Korea, Sudan, Syria and some other regions.

ຕິດຕໍ່ພວກເຮົາ

ຕິດຕໍ່ພວກເຮົາ